Strategy did not sell $1.25 billion of Bitcoin. It gave itself permission to do so, as part of a wider capital overhaul. The real driver of the stock is the premium to its Bitcoin holdings, and that premium has been shrinking.

Summary

- On June 29, 2026, Strategy’s board authorized a BTC Monetization Program allowing it to sell up to $1.25 billion of Bitcoin if needed, a cap and a framework, not a completed sale.

- The program is one piece of a new Digital Credit Capital Framework that also set up $2 billion of buybacks, $1 billion for common stock and $1 billion for preferred securities, and raised the STRC preferred dividend to 12%.

- Strategy holds 847,363 BTC bought for $64.10 billion, an average near $75,651 per coin, so the full $1.25 billion would be roughly 20,800 BTC, about 2.5% of its stack.

- The number that actually drives MSTR is mNAV, the premium the stock trades at relative to its Bitcoin holdings, and that premium has compressed toward 1x, which is why the company is pivoting from issuing equity to buybacks and selective Bitcoin sales.

- MSTR rose on the announcement even with Bitcoin near $60,000, but the forecast hinges on whether the premium can hold and where Bitcoin goes, not on the sale authorization itself.

The headline that traveled fastest was wrong in a way that matters. Strategy did not sell $1.25 billion of Bitcoin. On June 29, 2026, its board authorized a program permitting the company to sell up to $1.25 billion of Bitcoin if it needs to, as one component of a broad overhaul of the financing model that has funded years of aggressive accumulation.

The distinction is the whole story: this is Strategy formalizing Bitcoin as a funding source it can tap, not a fire sale of its holdings. Whether that is bullish or bearish for the stock depends on a number most headlines never mention: the premium MSTR trades at over the Bitcoin it owns.

This piece lays out exactly what Strategy announced, why mNAV is the real driver of the stock, how the pivot from never-sell to active capital management changes the picture, whether selling Bitcoin helps or hurts MSTR, the buyback and dividend math, the stock’s leverage to Bitcoin, and what it all means for the forecast. It closes with bull, base, and bear scenarios and a short FAQ. Note at the outset: MSTR is a stock, and nothing here is investment advice.

What Strategy actually announced

The June 29 filing introduced a Digital Credit Capital Framework that ties together Strategy’s Bitcoin holdings, its preferred securities, and its equity. Its most-discussed component is the BTC Monetization Program, which authorizes the company to sell Bitcoin primarily to raise up to $1.25 billion for a USD Reserve, and also to fund preferred dividends, interest, and buybacks.

Any Bitcoin sales beyond those stated purposes or amounts would require additional board approval. In Strategy’s own framing, sales would happen from time to time depending on market conditions and capital needs, not on a fixed schedule.

The framework did more than open the door to Bitcoin sales. It set up a board-approved USD Reserve that stood at roughly $2.55 billion as of June 28, dedicated to covering preferred dividends and interest, with a policy that the reserve stay above 12 months of coverage.

It authorized 2 separate buyback programs of up to $1 billion each, 1 for the Class A common stock and 1 for the Digital Credit preferred securities, $2 billion in total repurchase capacity. And it raised the dividend rate on the STRC preferred stock to 12% from 11.5%, effective for record dates on or after July 1, a move aimed at pushing that security back toward its $100 par value.

Alongside the framework, Strategy also disclosed it had raised about $1.15 billion selling common shares through its at-the-market program, and that it had paused Bitcoin buying, holding steady at 847,363 BTC.

The picture, then, is a company building a cash cushion, arming itself to buy back its own securities, and giving itself the option to sell a slice of Bitcoin to fund all of it.

The number that actually matters: mNAV

To forecast MSTR, you have to understand mNAV, the modified net asset value, which is the relationship between the company’s market value and the value of its Bitcoin holdings. For years, MSTR traded at a large premium to its Bitcoin, meaning the market valued the company well above the worth of the coins on its balance sheet. That premium was the engine of the entire model.

When a company trades above the value of its assets, it can issue new shares at that premium and use the proceeds to buy more of the asset, adding more Bitcoin per share than the dilution costs. Issue high, buy Bitcoin, watch the premium justify more issuance: a reflexive flywheel that worked as long as the premium held.

The problem driving the June overhaul is that the premium has compressed toward 1x, meaning MSTR has been trading close to the bare value of its Bitcoin. At or near 1x, the flywheel stalls, because issuing equity no longer adds Bitcoin per share; it just dilutes. That is why Strategy explicitly said it intends to be disciplined about issuing common stock when the shares trade near 1x mNAV.

With the equity lever jammed, the company turned to the other tools: buy back securities to support their value, and monetize a small portion of Bitcoin to fund obligations rather than selling stock into a thin premium. Read this way, the $1.25 billion authorization is not a panic move. It is the logical response to a compressed premium.

For the stock price, the implication is direct. MSTR is, in large part, a leveraged claim on Bitcoin plus or minus a premium. Where that premium goes, expansion back toward the old multiples or further compression toward 1x or below, will drive the stock as much as Bitcoin itself does.

From never-sell to capital management

The symbolic weight of the announcement comes from what it ends. For years, Michael Saylor built Strategy around one rule: raise capital, buy Bitcoin, and do not sell. That doctrine was the company’s identity. It cracked on June 1, 2026, when Strategy disclosed its first Bitcoin sale since 2022, a token 32 coins, negligible against holdings worth tens of billions but enormous in what it signaled. The June 29 framework formalizes the shift, turning a one-off sale into a standing capacity to monetize Bitcoin as part of routine capital management.

The scale keeps it in perspective. Strategy holds 847,363 BTC acquired for $64.10 billion, an average cost near $75,651 per coin. The full $1.25 billion, if ever executed, would be roughly 20,800 BTC, about 2.5% of the stack. This is not the company unwinding its Bitcoin thesis.

Saylor framed the existing reserve plus the new monetization capacity as providing around $3.8 billion of dividend coverage, close to 26 months, while keeping the commitment to long-term Bitcoin exposure. The pivot is from accumulation at all costs to disciplined balance-sheet management, which is a meaningful change in character even if the Bitcoin pile barely moves.

Does selling Bitcoin help or hurt the stock?

This is the question the market is actually debating, and there is a real case on each side. The constructive read is that the framework strengthens the company. A funded USD Reserve and the ability to monetize Bitcoin mean preferred dividends and interest are covered without forced equity sales into a weak premium, which reduces a key risk that had been weighing on both the common and the preferred securities.

Buyback capacity gives the company a tool to support its own securities when they trade cheaply. And the discipline around issuing stock near 1x mNAV stops the dilution that erodes value when the premium is gone. In this reading, the overhaul removes overhangs, and the stock should breathe easier, which is roughly how it reacted on the day, rising on the announcement.

The bearish read is that the framework is a tacit admission the old model is broken. Selling any Bitcoin at all, after building a brand on never selling, removes the accumulation flywheel that justified MSTR’s premium in the first place. If the company is no longer a one-way Bitcoin accumulator, the argument for paying a premium over its holdings weakens, which could keep mNAV pinned near 1x or push it below.

There is also a market-wide angle: Strategy selling Bitcoin, even a small amount, adds supply and dents sentiment in a leveraged, reflexive way, since the company’s buying had helped push Bitcoin higher on the way up. In this reading, the overhaul manages decline rather than reversing it.

The honest answer is that both can be true at once: the framework reduces short-term financial risk while confirming the premium era is over. That combination is exactly why the stock can rise on the news and still face a lower ceiling than it once had.

The buybacks and the dividend math

The capital tools deserve a closer look because they shape the floor under the stock. The $2 billion in buyback authority, split between common and preferred, gives Strategy a mechanism to return capital and defend its securities when they trade below intrinsic value, which can support the share price at the margin. Buybacks are most accretive precisely when the stock trades near or below the value of its assets, so authorizing them at compressed mNAV is internally consistent with the discipline message.

On the dividend side, raising the STRC rate to 12% is aimed at pushing that preferred security back toward its $100 par value, a sign the company is prioritizing the health of its credit stack. The USD Reserve at roughly $2.55 billion covers about 17 months of preferred dividends and interest on its own, with a policy floor of 12 months, and the reserve combined with the Bitcoin monetization capacity extends coverage to around 26 months by Saylor’s account.

That coverage is the point of the whole exercise: it buys time and reduces the chance of a forced, dilutive capital raise at the worst possible moment. For the common stock, a more stable credit structure underneath is a quiet positive, even if it is less exciting than the accumulation story it replaces.

The leverage to Bitcoin

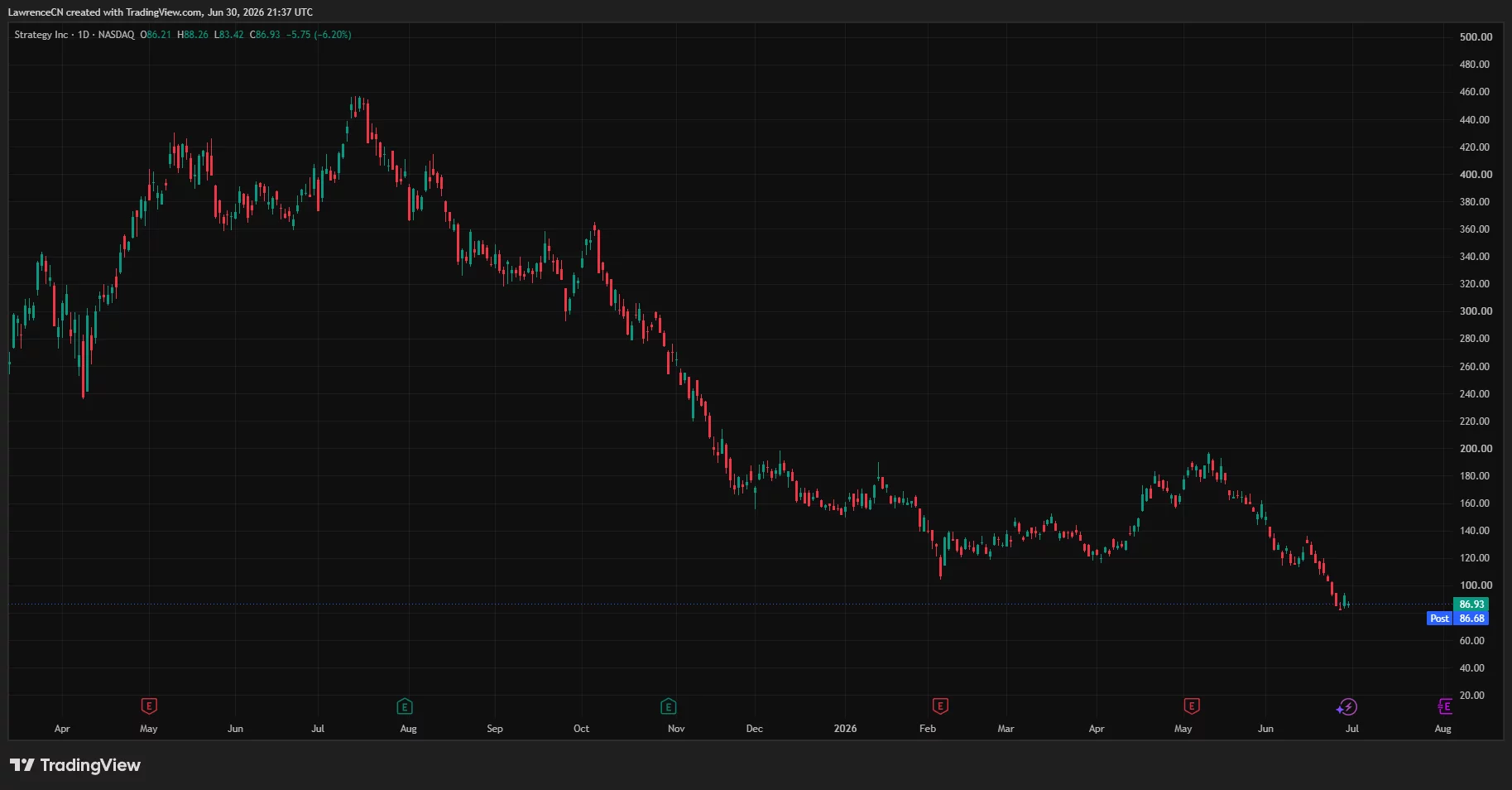

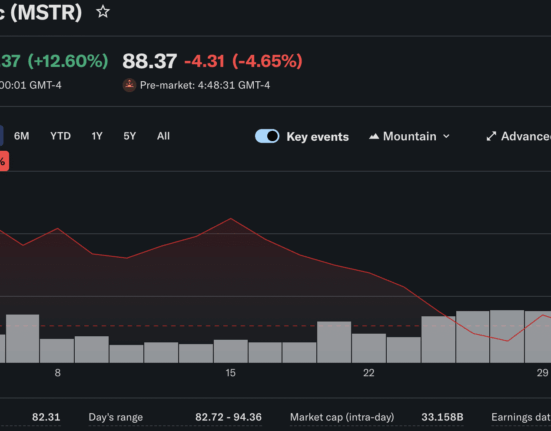

Whatever happens with the premium, MSTR remains a high-beta proxy for Bitcoin, and Bitcoin is the larger variable. With Bitcoin near $60,000 as of late June, down sharply from its prior highs, Strategy’s average cost near $75,651 means a meaningful portion of the stack sits underwater on paper, which is part of the pressure that prompted the overhaul. The stock tends to move more than Bitcoin in both directions, so the Bitcoin path dominates the forecast.

If Bitcoin recovers, the value of the holdings rises, the premium has more room to expand, and the leveraged nature of the stock can produce outsized gains. If Bitcoin stays soft or falls further, the holdings lose value, the pressure on the credit structure grows, and the monetization program may be used more actively, which feeds the bearish reflexivity. In short, the $1.25 billion authorization changes how Strategy manages its balance sheet, but it does not change the fact that the single biggest input to MSTR’s price is where Bitcoin trades.

What it means for the MSTR forecast

Forecasting a stock like MSTR is not the same as forecasting a token, and it would be irresponsible to attach a precise price target to a security whose value depends on two moving parts, the Bitcoin price and the mNAV premium, that interact reflexively.

The useful framing is conditional. MSTR’s value can be thought of as the value of its Bitcoin per share, multiplied by whatever premium or discount the market assigns. The June overhaul mainly affects the premium term: by reducing forced-dilution risk and adding buybacks, it supports the premium at the margin, while the end of never-sell may cap how high that premium can climb. The Bitcoin term is set by the market.

That is why the scenarios below are built around those 2 drivers rather than a single number. They are illustrative, not predictions, and they are not advice.

How the flywheel worked, and why it stalled

To see why the June overhaul was necessary, it helps to trace the mechanism that built Strategy in the first place. The company would issue new securities, common stock, convertible debt, or preferred shares, and use the proceeds to buy Bitcoin.

Because the market valued MSTR above the worth of its Bitcoin, each issuance added more Bitcoin per share than it diluted away, so existing holders came out ahead even as the share count grew. More Bitcoin per share supported the premium, the premium justified more issuance, and the cycle compounded. For years this reflexive loop turned a software company into the largest corporate holder of Bitcoin on the planet, with 847,363 coins acquired for $64.10 billion.

The loop only works in one direction, and only above a certain line. That line is roughly 1x mNAV, the point where the stock trades at the bare value of its Bitcoin. Above it, issuing stock is accretive and the flywheel spins. At or below it, issuing stock is dilutive, because the company would be selling shares for less than the Bitcoin those shares represent, handing value to new buyers at the expense of existing holders.

When the premium compressed toward 1x in 2026, the most powerful tool in Strategy’s kit, the ability to print equity and buy Bitcoin, stopped being usable without harming shareholders. The flywheel did not just slow. It hit a wall.

That is the context that makes the new framework coherent. With the equity lever jammed, the company reached for the tools that work at a compressed premium: buying back its own securities when they trade cheaply, raising a cash reserve so it is not forced to issue stock at the wrong price to cover dividends, and giving itself the option to monetize a small slice of Bitcoin to fund those obligations. Each piece is a response to the same problem. The premium that powered everything is gone, so the company is building a structure that can function without it.

What to watch: the signals that move MSTR

For readers tracking MSTR instead of the daily noise, a few signals will indicate which scenario is taking shape. The first is Bitcoin’s price relative to Strategy’s roughly $75,651 average cost. While Bitcoin trades near $60,000, a meaningful portion of the stack sits underwater on paper, which keeps pressure on the credit structure. A recovery above the cost basis would ease that pressure and give the premium room to expand; further weakness would deepen it.

The second is the direction of mNAV itself. A premium rebuilding above 1x would signal the market is again willing to pay up for Strategy’s structure, the bullish path. A premium stuck at 1x or slipping to a discount would confirm the de-rating the bears expect.

The third is the pace of actual Bitcoin sales under the new program: sparing, opportunistic use would read as disciplined capital management, while heavy or frequent sales would read as forced and would reinforce the broken-model narrative. The fourth is buyback execution, whether the company actually repurchases common and preferred securities into weakness, which would support prices and show the framework is more than words.

The fifth is the health of the preferred stack, with the STRC dividend raised to 12% to push that security toward its $100 par and the reserve policy holding above 12 months of coverage. Stability there underpins the whole structure; stress there would signal trouble spreading.

Tracked together, these five map the two variables that decide the stock, the Bitcoin price and the premium, onto observable events. The $1.25 billion authorization changed Strategy’s toolkit. These signals will show whether the tools are working.

Bull, base, and bear scenarios for MSTR

The scenarios combine the Bitcoin path with the direction of the mNAV premium. They describe possible outcomes, not targets, and the figures are deliberately framed as conditions instead of prices.

Bull case

In the bull scenario, Bitcoin recovers from the $60,000 area, lifting the value of Strategy’s 847,363 coins back above the cost basis and easing the pressure that prompted the overhaul. The buybacks and the funded reserve reassure the market that the credit structure is sound, dilution risk fades, and investors regain confidence enough to pay a premium over net asset value again. mNAV expands back above 1x, and because MSTR is leveraged to both Bitcoin and its own premium, the stock outpaces Bitcoin to the upside. This case needs Bitcoin strength and a restored willingness to pay up for Strategy’s structure.

Base case

In the base scenario, Bitcoin chops sideways around current levels and the premium stays compressed near 1x. The framework does its job of stabilizing the credit stack and removing forced-sale risk, so the stock avoids a crisis, but with the accumulation flywheel gone, MSTR trades largely in line with the value of its Bitcoin, give or take a modest premium. The buybacks provide some support, the monetization program is used sparingly, and the stock tracks Bitcoin without the old multiplier. This is the “stabilized but de-rated” outcome where MSTR behaves more like a leveraged Bitcoin holding company than a premium growth story.

Bear case

In the bear scenario, Bitcoin weakens further from $60,000, pushing more of the stack underwater and forcing more active use of the monetization program to cover obligations. The market reads continued Bitcoin sales as confirmation the model is broken, mNAV slips below 1x to a discount, and the leveraged downside takes the stock lower than Bitcoin’s decline alone would suggest. Preferred-stack stress, despite the higher STRC dividend and the reserve, keeps sentiment fragile. In this case, the overhaul slows the bleeding without stopping it, and the stock re-rates toward or below the value of its Bitcoin.

Frequently Asked Questions

Did Strategy actually sell $1.25 billion of Bitcoin?

No. On June 29, 2026, Strategy’s board authorized a program permitting it to sell up to $1.25 billion of Bitcoin if needed, primarily to fund a USD Reserve and service obligations. It is a cap and a framework, not a completed sale. Any sales would happen over time depending on conditions, and selling beyond the stated purposes would require further board approval.

What is mNAV and why does it matter for MSTR?

mNAV, or modified net asset value, is the premium or discount at which MSTR trades relative to the value of its Bitcoin holdings. A premium lets Strategy issue stock and buy more Bitcoin accretively, powering its growth. That premium has compressed toward 1x, which jams the equity lever and is the core reason for the new buyback and Bitcoin-monetization tools. Where the premium goes is a primary driver of the stock.

How much Bitcoin does Strategy hold?

As of late June 2026, Strategy held 847,363 BTC purchased for an aggregate $64.10 billion, an average near $75,651 per coin. The full $1.25 billion monetization authorization would represent roughly 20,800 BTC, about 2.5% of the holdings. The company paused Bitcoin buying in the week of the announcement.

Is the announcement good or bad for the stock?

It is genuinely mixed. The framework reduces forced-dilution risk, funds dividends, and adds buyback capacity, which the market read positively on the day. But formalizing Bitcoin sales ends the never-sell model that justified MSTR’s premium, which may cap how high the premium can climb. Both effects can hold at once: lower near-term risk, lower long-term ceiling.

How does Bitcoin’s price affect MSTR?

MSTR is a high-beta proxy for Bitcoin and tends to move more than Bitcoin in both directions. With Bitcoin near $60,000, below Strategy’s average cost, part of the stack is underwater on paper. A Bitcoin recovery would lift the holdings and give the premium room to expand, while further weakness would deepen the pressure and could trigger more active Bitcoin monetization.

What is the STRC dividend change about?

Strategy raised the dividend on its STRC preferred stock to 12% from 11.5%, effective for record dates on or after July 1, 2026. The goal is to push the security back toward its $100 par value and signal commitment to the health of its preferred, or Digital Credit, stack. It is part of the broader framework aimed at stabilizing the company’s capital structure.

Disclaimer: This article is for information purposes only and does not constitute financial, investment, or trading advice, and the author is not a licensed financial adviser. MSTR is a publicly traded stock whose value depends on volatile inputs including the price of Bitcoin. Price scenarios are illustrative and speculative, not predictions or recommendations. Always do your own research and consider consulting a licensed professional before making financial decisions. Figures are accurate as of June 30, 2026, and will change.

Leave feedback about this